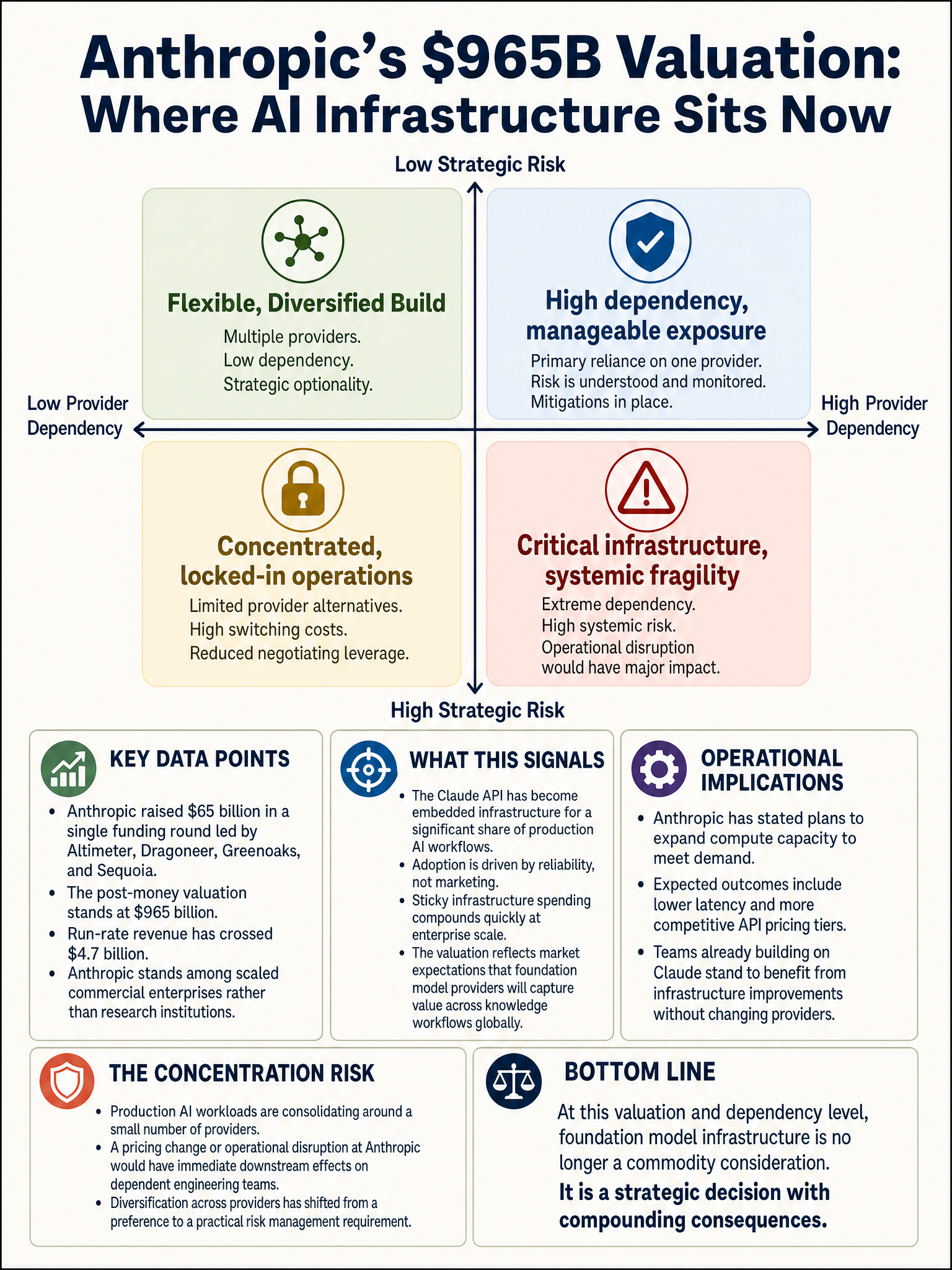

Anthropic raises $65B Series H at $965B valuation, run-rate revenue crosses $4.7B

Anthropic Just Crossed $4.7B in Run-Rate Revenue. The Market Believes It.

There are valuations that make you squint, and then there is whatever Anthropic just did. A $65 billion Series H round, led by Altimeter, Dragoneer, Greenoaks, and Sequoia, at a $965 billion post-money valuation. That puts Anthropic within breathing distance of a trillion dollars before it has filed for an IPO. I have been watching this space for a while now, and that number still makes me stop.

The same week that round was announced, Anthropic posted that run-rate revenue crossed $4.7 billion. That is not a projection. That is money coming in the door, consistently enough to annualize it.

These two numbers together tell a specific story, and it is worth pulling apart.

Why Enterprises Are Locking In on Claude

The revenue growth is not driven by consumers tinkering with chatbots. Anthropic said directly that it has been driven by organizations across many industries deploying Claude in their core operations. That phrase, “core operations,” matters. It means production workflows, not pilots.

The Claude API has earned a reputation among engineering teams for reliability and instruction-following precision. When something works well enough that you stop evaluating alternatives, you integrate deeper. You build more on top of it. The switching costs compound quietly, and the revenue follows.

This is classic infrastructure stickiness. It is the same dynamic that kept AWS dominant long after its competitors caught up on features. When you are embedded in production, you are very hard to displace.

What $965B Actually Implies

The valuation-to-revenue multiple here is roughly 200x annualized revenue. That is not a number you justify with current financials alone. Investors at this level are pricing in a specific belief: that Anthropic captures a durable, large share of enterprise AI spend over the next decade, and that the margin profile of that business improves significantly as it scales.

I think they are probably right about the direction, though 200x multiples leave almost no room for execution stumbles. The compute costs alone at this scale are not trivial, and the gap between run-rate revenue and profitability is real.

That said, the investor list is not made up of tourists. Sequoia has seen this pattern before. When firms at that level move this aggressively, they are not making a hope trade.

The Safety Angle Is Quietly Becoming a Revenue Feature

Something I do not see discussed enough: Anthropic’s safety positioning is starting to look like a competitive differentiator in regulated industries. Anthropic co-founder Chris Olah was invited to speak at the presentation of Pope Leo XIV’s encyclical “Magnifica humanitas” this week, which is a genuinely unusual signal about where the organization sits culturally. Enterprise buyers in healthcare, finance, and government care deeply about who built the model and what values shaped it.

That reputation is not accidental, and it is not free marketing. It converts.

Separately, Anthropic published a piece this week on its engineering blog about agent sandboxing and permission scoping, laying out how it thinks about limiting the blast radius of agentic mistakes. That kind of public technical transparency builds trust with the engineering teams who are actually making procurement decisions.

Where This Leaves Everyone Else

OpenAI is still the volume leader and the brand most consumers recognize. Google has distribution, infrastructure, and a serious research bench. xAI is competing on price with models like grok-build-0.1 at $1 per million input tokens, which is genuinely aggressive. Mistral is deploying into Airbus, BMW, and EDF in production environments.

The market is not winner-take-all. But a $965 billion valuation suggests that at least one very large pool of capital believes Anthropic is not just participating, it is setting terms.

If they can close the gap between run-rate revenue and actual profitability while defending their enterprise footprint against Google’s distribution advantages, this valuation becomes a floor, not a ceiling.

That is a big if. But the $4.7 billion number means they are not building toward something hypothetical anymore.

Sources

#AI #Anthropic #MachineLearning #EnterpriseAI #Claude #VentureCapital #AIInfrastructure