Leopold Aschenbrenner’s contrarian AI infrastructure portfolio strategy and what it means for engineers thinking about the physical constraints of AI

The Bet Behind the Bet: What Leopold Aschenbrenner’s Portfolio Tells Engineers About AI’s Real Constraints

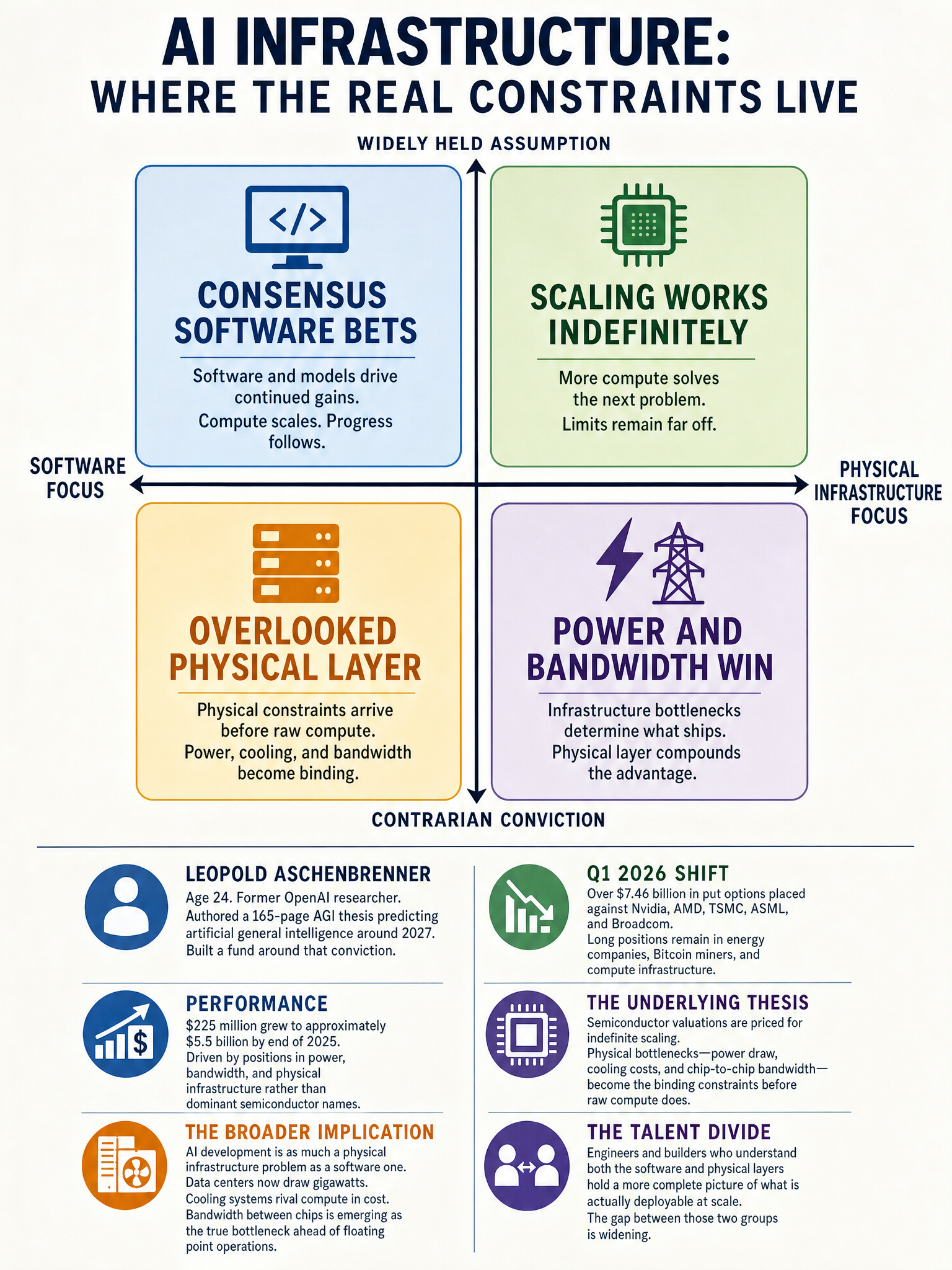

Most people covering AI are watching the model benchmarks. Aschenbrenner watched the power grid.

That difference in focus is what turned $225 million into roughly $5.5 billion by the end of 2025, and then into $13.67 billion by Q1 2026. I’ve been skeptical of fund manager narratives before, but this one is hard to dismiss, because the thesis was written down before the trades were made. You can actually check the logic.

The Physical Layer Is the Moat

When Aschenbrenner launched his fund after getting fired from OpenAI in April 2024, he made a deliberate choice to ignore the obvious plays. Zero Nvidia. Zero Microsoft. Zero Google. Zero Amazon. Instead he went long on the things AI physically cannot run without: power generation, bandwidth, storage, and compute infrastructure.

Bloom Energy returned 1,422%. Lumentum 1,331%. SanDisk 3,130%. IREN 583%. These aren’t rounding errors.

His argument, spelled out in a 165-page document, was that AI’s constraints aren’t algorithmic, they’re physical. You can write better transformer architectures all day, but if you don’t have the power to run them or the storage to feed them, the software doesn’t matter. The market was pricing AI as a software story. He priced it as a civil engineering story. He was right.

🔋

What Q1 2026 Actually Says

Here’s where it gets genuinely interesting for anyone thinking about where the money flows next.

His Q1 2026 SEC filing shows $7.46 billion in put options against the semiconductor stack. Nvidia puts at $1.57B. Broadcom at $1.01B. AMD at $969M. TSMC at $535M. ASML at $494M. That is not a hedge position. That is a directional bet that the most crowded AI trade in the market has over-extended.

But he didn’t sell his infrastructure longs. Bloom Energy is still in at $878M. SanDisk at $724M. CoreWeave at $556M. He also added call options on Micron ($422M), SanDisk ($388M), and TSMC ($354M).

Read that carefully. He holds puts on TSMC and calls on TSMC simultaneously. That’s not confusion, that’s a spread. He thinks TSMC’s near-term expectations are inflated but its long-term position in the AI buildout is real.

The thesis evolved from “AI wins” to something more specific: the physical buildout of AI continues, but the companies the market bid up as AI proxies may have already absorbed too much optimism into their prices.

What This Means If You’re Building

I think about this from an engineering perspective more than a financial one. The pattern Aschenbrenner identified, physical constraints being systematically underpriced while software-layer winners get overcrowded, is the same pattern that plays out inside companies.

Engineering teams obsess over model selection and fine-tuning while their inference costs are quietly eating the budget. They chase benchmark improvements while their storage I/O is the actual bottleneck. The capital markets made the same mistake at scale, and someone made billions noticing it.

The companies he’s still long on, CoreWeave, Bitcoin miners repurposed as compute infrastructure like IREN and Riot and CleanSpark, power infrastructure plays, these are the teams running the physical plant. They’re not glamorous. They don’t get conference keynotes. But if you actually believe AGI is coming by 2027, as Aschenbrenner does, then the boring infrastructure underneath it is where you want to be, because demand for it doesn’t depend on which lab wins.

⚡

The Prediction Embedded in the Puts

The semiconductor put position implies something specific. Either chip demand softens as AI spending consolidates around fewer, more efficient models, or the current valuations on companies like Nvidia and ASML have already priced in a future that takes longer to arrive than the market expects.

Given that model efficiency has been improving faster than most people anticipated, the first option isn’t crazy. Fewer chips needed per unit of capability is deflationary for the semiconductor supply chain, even if total AI compute demand grows. Aschenbrenner may be betting that the efficiency curve hits before the next big demand wave does.

That’s a sophisticated and falsifiable prediction. I respect falsifiable predictions.

Whether he’s right about the timing on semiconductors, I don’t know. But the underlying framework, price the physical constraints, not the software narrative, has already proven itself once. Engineers building AI systems would do well to apply the same lens to their own architecture decisions. The bottleneck is almost never where the hype is.

Sources & Further Reading

#AIInfrastructure #MachineLearning #AIEngineering #TechInvesting #LeopoldAschenbrenner